Transunion Monitoring & Credit Vision

COVID’s impact on the world has been all-encompassing. It has affected our actions, our thought processes, changed our habits, increased our awareness, and required those in the lending space to rethink how they operate under these adverse conditions as well as the implications the CARES Act has brought to their business.

The pandemic’s impact on a consumer’s employment and financial situations has and will continue to work its way into the reporting to the national CRAs. Accordingly, lenders need to effectively identify this information and make the appropriate modifications to their credit strategies across the full credit lifecycle of their customers. The volume of reported modifications has also increased dramatically.

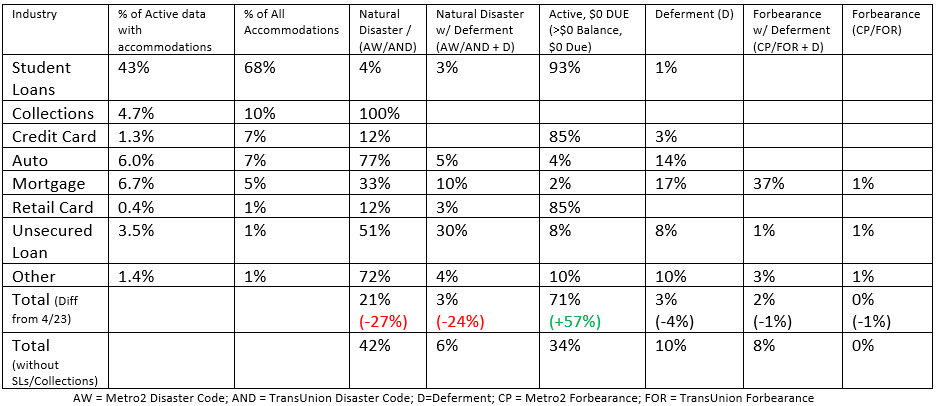

According to TransUnion’s statistics: “There is industry variability in both the volume of accommodations and reporting strategies being used along with shifting of strategies from April to May reporting. Note: Metrics based on the difference between 2/29/20 and 5/17/20 snapshots of TransUnion’s credit file “active trades”.

These metrics were designed to give a broad view into the types of COVID-19 reporting strategies being used by the industry, along with the degree of variability in volumes by industry and variability, within the various reporting strategies.

Additional information included shows how reporting strategies shifted from April to May. “Diff from 4/23” percentage change to the ‘Total’ shows how reporting strategies shifted from 4/23 to 5/17. This was largely driven by student loans shifting from ‘Natural Disaster w/ Deferment’ to ‘Active, $0 Due’ but we were seeing a more gradual shift from the explicit codes (natural disaster, deferment, forbearance) to ‘Active, $0 Due’ before the May student loan reporting.

As it relates to credit bureau reporting, three types of reporting scenarios have come to light. Different possible scenarios include:

- Standard – Consumer requests accommodations and the Lender uses the Forbearance code.

- Non-Standard – Consumer requests accommodations but the Lender does not use the Forbearance code but may use some other reporting option.

- Unknown – The consumer does not request or know to request accommodations, but the lender provided payment relief to the entire portfolio.

Creditors should be aware of how the crisis is affecting the information and look at new information that may help to assess the consumer’s ability to pay and their ability to resume payments once the crisis is over. There are several ways to do that.

One area for available data is utilizing trended data. CreditVision’s trended data elements give insight to:

- Balance trends

- Utilization patterns

- Changes in open-to-buy

- Payment data

- Address history

Using balance trends and utilization patterns, lenders can gain insight into a consumer’s ability to pay. Since forbearance or deferred payment data normally show a $0.00 amount under the Disaster coding requirements (see Metro 2 formatting), understanding payments prior to accommodations are essential and trended data offers a more holistic view of the consumer’s payment patterns and credit utilization.

A second area to consider for additional data is the attributes provided by the bureaus. TransUnion’s “CreditVision Acute Relief Attributes help identify consumers impacted by acute economic conditions – enabling support strategies to be adjusted if necessary.” Attributes provide an additional look at the consumer information to determine the current amount of debt that is being affected by the disaster codes. This includes attributes such as the total balance of tradelines affected, the number of open trades affected, trades affected delineated by industry type such as those mentioned in the chart above. This set of 88 non-adverse actionable CreditVision Attributes identifies consumers who have been reported with a disaster code. A creditor can incorporate this information into their current models or route applications that include these indicators through a revised credit path such as to their underwriting workflow system for manual verification.

A third option for gaining awareness on how the crisis is affecting creditors portfolios is to incorporate Account and Portfolio Monitoring services.

An Account Monitoring program is used to proactively evaluate the payment behavior of your customers allowing you to implement more appropriate collections strategies not only related to your delinquent account but also your current account. As it relates to current accounts, delinquency movement on other reported tradelines can be used to trigger an early collection call or text to get ahead of any upcoming delinquency on your account. Treatment strategies on delinquent accounts can be adjusted to reflect the overall payment behavior of the account helping optimize the use of your most expensive recourse, labor.

Portfolio Monitoring includes “the capability to monitor your debt portfolio for changes to a custom set of data points crucial to your business. Through this functionality, you can proactively address changes in your book of business and restructure your collections priorities. Portfolio monitoring allows companies to have greater control over inventory as well as:

- Avoid compliance risk. Every debt portfolio contains inventory protected by state and federal laws.

- Foster healthy margins. The business climate for third-party collectors has seen profit margins drop to all-time lows. Portfolio monitoring helps to maximize your current resources and boost recoveries.

- Foster more recoveries.By enabling collectors to be more focused on those accounts that are recoverable, you can maximize your profit margin.”

Account and Portfolio monitoring is helpful to keep ahead of the continued economic impacts of this crisis as well as being able to better predict the changing habits of consumers as quarantines and cities remain less than fully operational.

TransUnion has kept ahead of the curve and continues to offer up to date information on their website and through their product updates. Please visit their website where you can find information on their CreditVision® Acute Attributes, Account Monitoring, Portfolio Monitoring and where you can find valuable statics from their monthly “Consumer Financial Hardship” studies.

GDS Link’s Modellica Analytical Services leverage industry-leading expertise that ensures risk managers maintain a comprehensive view of the financial landscape and the agility to adapt to change. Connect with one of our Solution Specialists to see how you can leverage your data to its full potential: