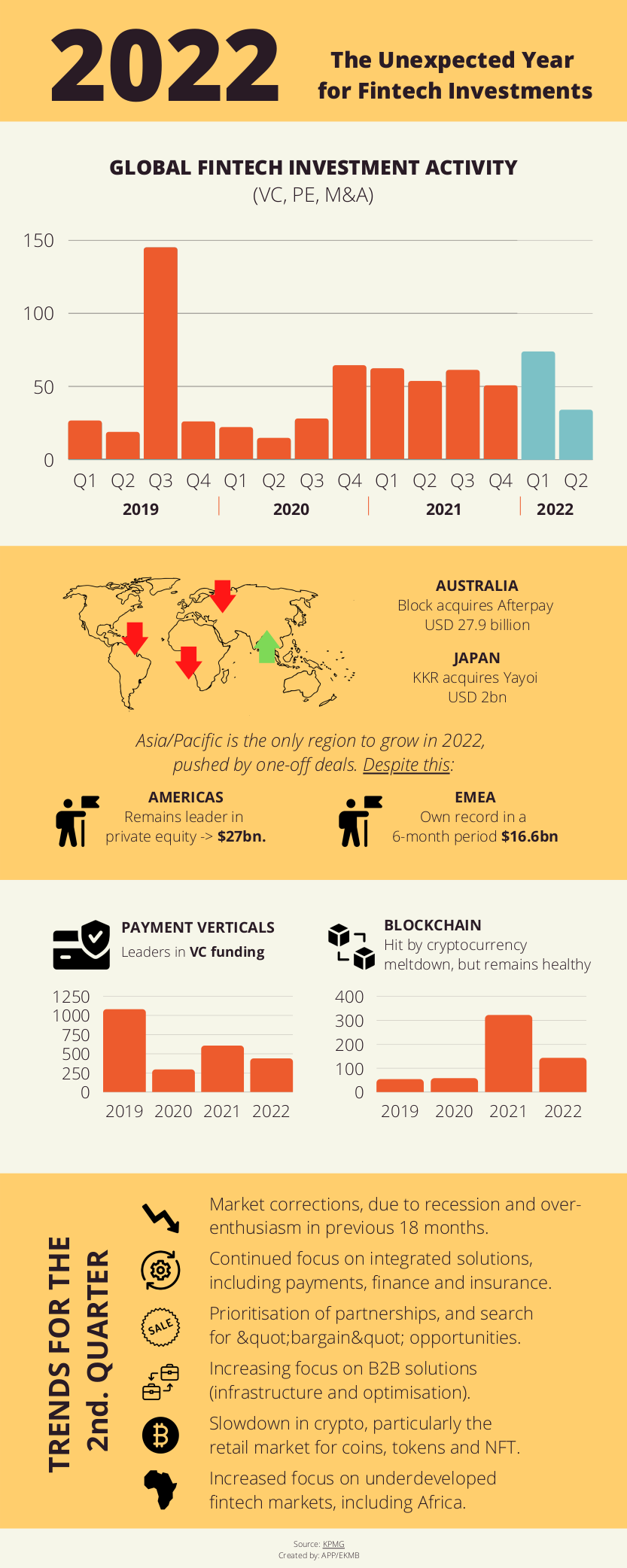

“Unexpected. That is the precise term chosen by the renowned Big Four firm KPMG to describe the year in terms of venture capital investments and other financial transactions in the Fintech sector. It does so in its recently published report

Fintech Pulse in the first half of the year. It chooses the term “unexpected” insofar as the figures are by no means positive, but neither can they be said to be decidedly negative. And also because it is a development that has taken place in contexts that were, a priori, unpredictable at the beginning of the year: the war in Ukraine, the stock market crash of cryptocurrencies, and the threat of recession knocking at the door incessantly.

“The optimism that pervaded the fintech market at the end of 2021 was quickly transformed,” reads the executive summary of this report, as supply chain challenges, rising inflation and rising interest rates, identified by government agencies as consequences of the conflict in Eastern Europe, were added to the usual uncertainties.

What is certain is that the raw data are, in principle, discouraging: both total global fintech investment and the total number of deals fell between H2 2021 and H1 2022. Indeed, it fell in the Americas and EMEA (Europe, Middle East and Africa), but Asia-Pacific saw a rise, albeit driven by one-off deals such as the $27.9bn Block-Afterpay deal in Australia.

Despite these figures, there is also reason for some uneasy calm. For example, America remains the leading investment region, which speaks to the fact that the hecatomb has not been total. Or the fact that despite the downturn, over the 12 months since 1 July 2021, the EMEA region has seen 6 months in a row with a turnover of more than $16 billion, a record high for its fintech venture capital history.

Some of the trends in Q1 and Q2 2022 have been:

- – Declining investment in most regions.

- – Cancellation of IPOs, following turmoil in the public markets and rapidly falling valuations.

- – Continued strength in the payments sector (fintech verticals).

- – Growing focus on automation and extreme automation in cybersecurity.

- – Growing diversity of countries (“jurisdictions”) attracting fintech investments, particularly venture capital rounds of over $100 million.

All of this, as well as the outlook for the second half of the year, is discussed in the infographic attached to this article, which we recommend, as usual, that you read the full report in its entirety.